Are you an employer who agrees a net pay arrangement with their employees? This net pay arrangement means that you as an employer guarantees that an employee will receive the same amount of pay every pay day.

Are you an employer who agrees a net pay arrangement with their employees? This net pay arrangement means that you as an employer guarantees that an employee will receive the same amount of pay every pay day.

This creates a financial risk to your business because there is no way you can know how much that pay will cost you.

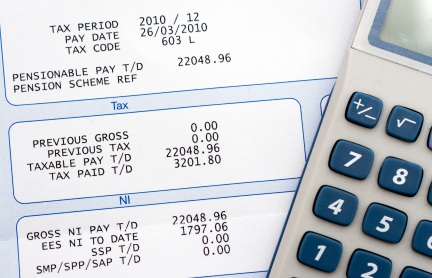

Generally employees can earn an amount every week, month or year which is tax free. In the current tax year (2018-19) that amount is £11,850 per year, or£988 per month or £228 per week. The tax code 1185L is the standard tax code and gives employees on this tax code the tax free allowance for the year.

A different tax code will give an employee a different tax free allowance. A lower tax code will mean less tax free allowance and a higher tax code will give a greater tax free allowance.

If an employee has other income which is taxable, receives or has received taxable benefits or has tax arrears they will not have the standard tax code of 1185L. They will most likely have a lower tax code.

So if you agreed to pay your employee £12,000 per year they would be taxed on just £150 of that earnings and you would have to pay them more than £12,000 to cover the tax. If the employee had a lower tax code, say 900L, because HMRC are recovering tax on other income, benefits or arrears you would have to pay them a lot more than £12,000 per year because only £9,000 of their income would be tax free. In the first scenario it would cost you an extra £30 per year but in the second it would cost you an extra £600.

Not only that, you would also be covering their employee's National Insurance contributions and their pension contribution. Pension contributions increase to 5% for employees on qualifying earnings from April 2019.

So as you can see, agreeing to a net pay arrangement with your employee can prove extremely costly. You won't be able to work out how much it will actually cost you in Gross Pay, tax, NI and pension contributions until your employee starts and you know what their tax code is.

The cost of taking on an employee at say £24,000 gross per year (£2,000 per month) would be £24,000 plus 13.8% NIC on earnings above the NIC threshold, plus 3% pension contribution on qualifying earnings. That equates to a total employer cost of approximately £26,570.

The cost of taking on an employee at say £24,000 gross per year (£2,000 per month) would be £24,000 plus 13.8% NIC on earnings above the NIC threshold, plus 3% pension contribution on qualifying earnings. That equates to a total employer cost of approximately £26,570.

An employee who has agreed a net pay of £24,000 per year (£2,000 per month) will cost an additional 12.8% NICs and 5% pension contributions equating to an extra £2,694 per year. The total cost for this net pay arrangement to the employer would be £29,263, £2693 more than it would cost normally.

This calculation shows the difference in the cost to your business of offering a gross salary and a net salary. And, of course, if your employee does not have a standard tax code the second option could cost you significantly more as you would be covering the extra tax HMRC are recovering and you would be paying higher NICs and pension contributions because their gross pay would be higher.

There are still employers who agree to a net pay amount. Maybe its because they can plan for a regular amount going out of the bank and can manage their cash flow but it can seriously affect the health of your business because the actual cost could become more than you can manage.

My advice is never to agree a net pay arrangement. Once you do you will never be able to change to a gross pay arrangement with an employee without seeking HR advice.